Application of Variance Decomposition Model in Pricing Analysis of Agriculture Commodity Spot and Future Market

Article Sidebar

Main Article Content

Abstract

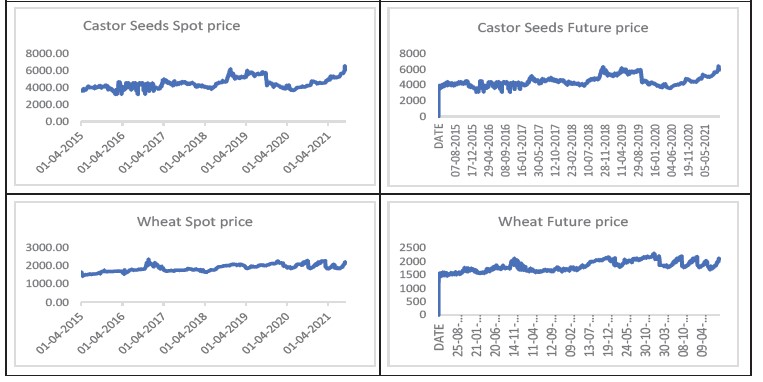

India's commodity markets are expanding quickly because of globalisation, which began in earnest in 1991. These markets underwent significant evolution in conjunction with other financial markets due to changes in legislation, such as SEBI controlling regulation of commodity market of India in 2015. The objective of the paper is to compare spot and futures pricing to seek price discovery for the selected commodities, which were only used in the agricultural industries. The present paper emphasized the causality direction amongst the spot-futures pricing. In this investigation, secondary quantitative data were used. The data was gathered through the website, annual reports, and the Bloomberg Database. The data was collected in the form of a time series with a daily frequency. The study covered a variety of agricultural goods, including guar gum, chana, guar seed, jeera, coriander, soybean, barley, turmeric, castor seed and wheat. A VAR model and models for variance decomposition are applied to analyze data. The empirical analysis demonstrated that spot markets controlled most agricultural commodities when compared to their future markets. Any new information that affected market pricing for agricultural commodities was reflected in the spot prices, which also affected the pricing of the commodities in the future.

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.

CC BY-NC-SA 4.0

Attribution Non-Commercial Share-alike 4.0 International

Visit here for more details: https://creativecommons.org/licenses/by-nc-sa/4.0/

References

Ali, J., & Gupta, K. B. (2011). Efficiency in agricultural commodity futures markets in India: Evidence from cointegration and causality tests. Agricultural Finance Review, 71, 162–178. https://doi.org/10.1108/00021461111152555

Andreasson, P., Bekiros, S., Nguyen, D. K., & Uddin, G. S. (2016). Impact of speculation and economic uncertainty on commodity markets. International Review of Financial Analysis, 43, 115–127.

Arouri, M. E. H., Hammoudeh, S., Lahiani, A., & Nguyen, D. K. (2013). On the short-and long-run efficiency of energy and precious metal markets. Energy Economics, 40, 832–844.

Aslan, S., Yozgatligil, C., & Iyigun, C. (2018). Temporal clustering of time series via threshold autoregressive models: Application to commodity prices. Annals of Operations Research, 260, 51–77. https://doi.org/10.1007/s10479-017-2659-0.

Belousova, J., & Dorfleitner, G. (2012). On the diversification benefits of commodities from the perspective of euro investors. Journal of Banking & Finance, 36, 2455–2472.

Bohl, M. T., Siklos, P. L., Stefan, M., & Wellenreuther, C. (2020). Price discovery in agricultural commodity markets: Do speculators contribute? Journal of Commodity Markets, 18, 100092.

Bopp, A. E., & Sitzer, S. (1987). Are petroleum futures prices good predictors of cash value? The Journal of Futures Markets (1986–1998), 19(4), 705.

Bouri, E., Jaikh, N., & Roubaud, D. (2019). Commodity volatility shocks and BRIC sovereign risk: A GARCH-quantile approach. Resources Policy, 61, 385–392.

Brockman, P., & Tse, Y. (1995). Information shares in Canadian agricultural cash and cattle. Applied Economics Letters, 2(10), 335–338.

Brooks, C., Rew, A. G., & Ritson, S. (2001). A trading strategy based on the lead–lag relationship between the spot index and futures contract for the FTSE 100. International Journal of Forecasting, 17(1), 31–44.

Chan, K. (1992). A further analysis of the lead–lag relationship between the cash market and stock index futures market. Review of Financial Studies, 5, 123–152.

Chang, C. P., & Lee, C. C. (2015). Do oil spot and futures prices move together? Energy Economics, 50, 379–390.

Cheng, I. H., & Xiong, W. (2014). Financialization of commodity markets. Annual Review of Financial Economics, 6, 419–441. https://doi.org/10.1146/annurev-financial-110613-034432

Chhajed, I., & Mehta, S. (2013). Market behavior and price discovery in Indian agriculture commodity market. International Journal of Scientific and Research Publications, 3(3), 1–4.

Choy, S. K., & Zhang, H. (2010). Trading costs and price discovery. Review of Quantitative Finance and Accounting, 34(1), 37.

Dash, M., & Andrews, S. B. (2010). A study on market behaviour and price discovery in Indian commodity markets. Available at SSRN 1722770.

Debasish, M., & Kushankur, D. (2011). Volatility and spill over effects in Indian commodity markets: A case of pepper. Studies in Business and Economics, 6(3), 119–145.

Easwaran, R. S., & Ramasundaram, P. (2008). Whether commodity futures market in agriculture is efficient in price discovery?An econometric analysis. Agricultural Economics Research Review, 21, 337–344.

Elumalai, K., Rangasamy, N., & Sharma, R. K. (2009). Price discovery in India’s agricultural commodity futures markets. Indian Journal of Agricultural Economics, 64, 315–323.

Frankel, J. A., & Rose, A. K. (2010). Determinants of agricultural and mineral commodity prices. In Inflation in an era of relative price shocks. Reserve Bank of Australia.

Garbade, K. D., & Silber, W. L. (1983). Price movements and price discovery in futures and cash markets. The Review of Economics and Statistics, 65, 289–297. https://doi.org/10.2307/1924495

Grossman, S. J. (1977). The existence of futures markets, noisy rational expectations and informational externalities. The Review of Economic Studies, 44(3), 431–449. https://doi.org/10.2307/2296900

Gupta, S., Choudhary, H., & Agarwal, D. R. (2018). An empirical analysis of market efficiency and price discovery in Indian commodity market. Global Business Review, 19(3), 771–789.

Hammoudeh, S., Dibooglu, S., & Aleisa, E. (2004). Relationships among US oil prices and oil industry equity indices. International Review of Economics & Finance, 13(4), 427–453.

Hasbrouck, J. (1995). One security, many markets: Determining the contributions to price discovery. The Journal of Finance, 50(4), 1175–1199.

Henriksen, T. E. S., Pichler, A., Westgaard, S., & Frydenberg, S. (2019). Can commodities dominate stock and bond portfolios? Annals of Operations Research, 282, 155–177. https://doi.org/10.1007/s10479-018-2996-7

Hernandez, M., & Torero, M. (2010). Examining the dynamic relationship between spot and future prices of agricultural commodities (No. 988). International Food Policy Research Institute (IFPRI).

Himanshu, H., Lanjouw, P., Murgai, R., & Stern, N. (2013). Nonfarm diversification, poverty, economic mobility, and income inequality: A case study in village India. Agricultural Economics, 44, 461–473.

Inani, K. S. (2018). Efficiency of Indian agricultural commodity futures market: An empirical investigation. Journal of Quantitative Economics, 16(1), 129–154.

Jena, S. K., Tiwari, A. K., Hammoudeh, S., & Roubaud, D. (2019). Distributional predictability between commodity spot and futures: Evidence from nonparametric causality-in-quantiles tests. Energy Economics, 78, 615–628.

Jiang, H., Todorova, N., Roca, E., & Su, J. (2017). Dynamics of volatility transmission between the U.S. and the Chinese agricultural futures markets. Applied Economics Letters, 49(34), 3435–3452.

Joseph, A., Sisodia, G., & Tiwari, A. K. (2014). A frequency-domain causality investigation between futures and spot prices of Indian commodity markets. Economic Modelling, 40, 250–258.

Joseph, A., Suresh, K. G., & Sisodia, G. (2015). Is the causal nexus between agricultural commodity futures and spot prices asymmetric? Evidence from India. Theoretical Economics Letters, 5, 285–295. https://doi.org/10.4236/tel.2015.52034

Karyotis, C., & Alijani, S. (2016). Soft commodities and the global financial crisis: Implications for the economy, resources and institutions. Research in International Business and Finance, 37, 350–359.

Kaura, R., Kishor, N., & Rajput, N. (2018). Price discovery and volatility spillovers: Evidence from non-agricultural commodity market in India. IUP Journal of Financial Risk Management, 15(3), 7–31.

Kawaller, I. G., Koch, P. D., & Koch, T. W. (1987). The temporal price relationship between S&P 500 futures and the S&P 500 index. The Journal of Finance, 42(5), 1309–1329.

Kolamkar, D. S. (2003). Regulation and policy issues for commodity derivatives in India. In S. Thomas (Ed.), Derivatives Market in India (pp. 207–210). Oxford University Press.

Kumar, B., & Pandey, A. (2013). Market efficiency in Indian commodity futures markets. Journal of Indian Business Research, 5(2), 101–121.

Kumar, S. (2004). Price discovery and market efficiency: Evidence from agricultural commodities futures markets. South Asian Journal of Management, 11(1), 32-47.

Lakshmi, V. D. M. V. (2017). Efficiency of futures market in India: Evidence from agricultural commodities. IUP Journal of Applied Economics, 16(3), 47-68.

Malhotra, M., & Sharma, D. K. (2013). Efficiency of GUAR SEED futures market in India: An empirical study. IUP Journal of Applied Finance, 19(1), 45-63.

Mattos, F., & Garcia, P. (2004). Price discovery in thinly traded markets: Cash and futures relationships in Brazilian agricultural futures markets. In Proceedings of the NCR-134 Conference on Applied Commodity Price Analysis, Forecasting and Risk Management. Retrieved from http://www.farmdoc.uiuc.edu/nccc134.

Mayer, H., Rathgeber, A., & Wanner, M. (2017). Financialization of metal markets: Does futures trading influence spot prices and volatility? Resources Policy, 53, 300–316.

McMillan, D. G., & Speight, A. E. (2001). Non-ferrous metals price volatility: A component analysis. Resources Policy, 27(3), 199–207.

Mukherjee, I., & Goswami, B. (2017). The volatility of returns from commodity futures: Evidence from India. Finance Innovation, 3(15).

Newberry, D. M. (1992). Futures markets: Hedging and speculation. In P. Newman, M. Milgate, & J. Eatwell (Eds.), The new Palgrave dictionary of money and finance (Vol. 2, pp. 207–210). Palgrave Macmillan.

Pati, P. C., & Padhan, P. C. (2009). Information, price discovery and causality in the Indian stock index futures market. IUP Journal of Financial Risk Management, 6(3–4), 7–21.

Pindyck, R. S. (2001). The dynamics of commodity spot and futures markets: A primer. The Energy Journal, 22(3), 1–30.

Pradhan, R. P., Hall, J. H., & du Toit, E. (2020). The lead–lag relationship between spot and futures prices: Empirical evidence from the Indian commodity market. Resources Policy, 101934.

Praveen, D. G., & Sudhakar, A. (2006). Price discovery and causality in the Indian derivatives market. ICFAI Journal of Derivatives Markets, 3(1), 22-29.

R. L., M., & Mishra, A. K. (2020). Price discovery and volatility spillover: An empirical evidence from spot and futures agricultural commodity markets in India. Journal of Agribusiness in Developing and Emerging Economies. doi:10.1108/JADEE-09-2019-0140

Raghavendra, R. H., Velmurugan, P. S., & Saravanan, A. (2016). Relationship between spot and futures markets of selected agricultural commodities in India: An efficiency and causation analysis. Journal of Business and Financial Affairs, 5(1), 2167–0234.

Rastogi, S., & Agarwal, A. (2020). Volatility spillover effects in spot, futures and option markets. Finance India, 34(1), 10114–10127.

Sahadevan, K. G. (2002). Price discovery, return and market conditions: Evidence from commodity futures markets. The ICFAI Journal of Applied Finance, 8, 25-39.

Schwarz, T. V., & Szakmary, A. C. (1994). Price discovery in petroleum markets: Arbitrage, cointegration and the time interval of analysis. The Journal of Futures Markets, 14(2), 147-167.

Sehgal, S., Rajput, N., & Deisting, F. (2013). Price discovery and volatility spillover: Evidence from Indian commodity markets. The International Journal of Business and Finance Research, 7(3), 57–75.

Sehgal, S., Rajput, N., & Dua, R. K. (2012). Price discovery in Indian agricultural commodity markets. International Journal of Accounting and Financial Reporting, 2(2), 22-44. doi:10.5296/ijafr.v2i2.2224.

Shah, A. (2002). Spatial poverty traps in rural India: An exploratory analysis of the nature of the causes. Journal of Social and Economic Development, 4, 123-147.

Shakeel, M., & Purankar, S. (2014). Price discovery mechanism of spot and futures market in India: A case of selected Agri commodities. International Research Journal of Business and Management, 8, 50–61.

Sharma, P., & Sharma, T. (2018). A study of the efficiency of Chili futures market in India. IUP Journal of Financial Risk Management, 15(3), 32–43.

Shree, B., & Singh, M. A. (2016). An analysis of past and present status of commodity derivatives market in India. International Journal of Advanced Research in Management and Social Sciences, 5(2), 163-184.

Singh, N. P., Shunmugam, V., & Garg, S. (2009). How efficient are futures market operations in mitigating price risk? An explorative analysis. Indian Journal of Agricultural Economics, 64, 324–332.

Srinivasan, P. (2012). Price discovery and volatility spillovers in Indian spot–futures commodity market. The IUP Journal of Behavioral Finance, 9(1), 70–85.

Stoll, H. R., & Whaley, R. E. (1990). The dynamics of stock index and stock index futures returns. Journal of Financial and Quantitative Analysis, 25(4), 441–468.

Talbi, M., de Peretti, C., & Belkacem, L. (2020). Dynamics and causality in distribution between spot and futures precious metals: A copula approach. Resources Policy, 66, 101645.

Thomas, S., & Karande, K. (2001). Price discovery across multiple spot and futures markets. IGIDR Finance Seminar Series.

Turnovsky, S. J. (1983). The determination of spot and futures prices with storable commodities. Econometrica: Journal of the Econometric Society, 51(5), 1363–1387.

Vasantha, G., & Mallikarjunappa, T. (2015). Lead-lag relationship and price discovery in Indian commodity derivatives and spot market: An example of pepper. IUP Journal of Applied Finance, 21(1), 71.

Wang, D., Tu, J., Chang, X., & Li, S. (2017). The lead–lag relationship between the spot and futures markets in China. Quantitative Finance, 17(9), 1447–1456.

Yang, J., Bessler, D. A., & Leatham, D. J. (2001). Asset storability and price discovery in commodity futures markets: A new look. Journal of Futures Markets, 21(3), 279–300.

Yang, J., & Leatham, D. J. (1999). Price discovery in wheat futures markets. Journal of Agricultural and Applied Economics, 31(3), 359–370.

Zapata, H. O., & Fortenbery, T. R. (1996). Stochastic interest rates and price discovery in selected commodity markets. Review of Agricultural Economics, 18(4), 643–654.